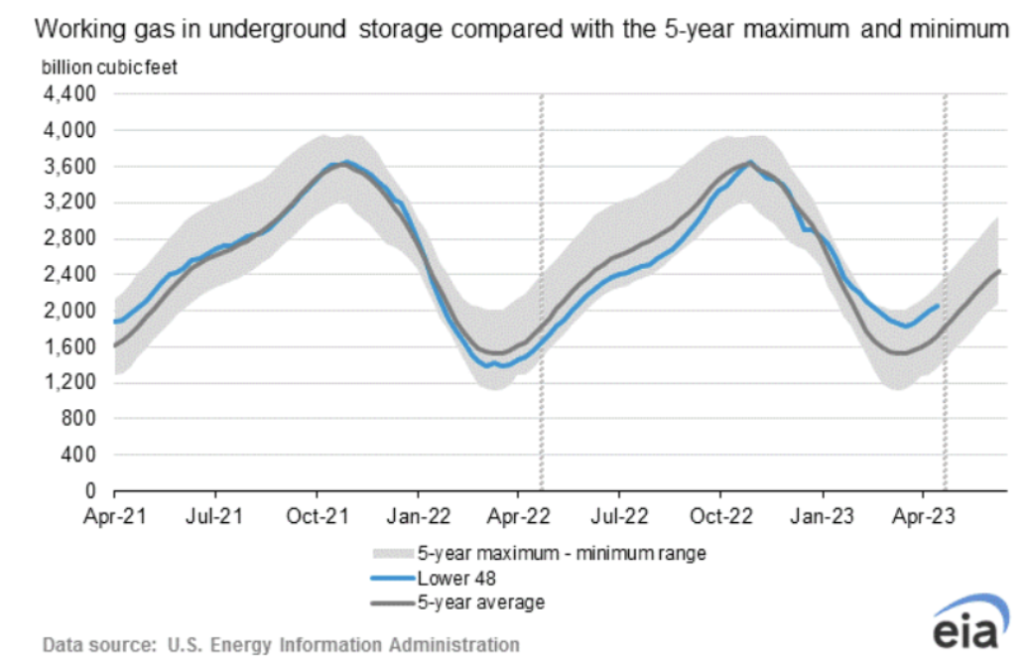

In the past year, Henry’s futures prices experienced a significant increase, exceeding $5 per MMBtu, and reaching a peak of over $9 in August. This caused some industry experts to speculate that the era of low-priced natural gas might be over as prices soared to levels not seen in over a decade. Nevertheless, as of April 14, the prompt month futures were valued at approximately $2.00 per MMBtu. This suggests that the market dynamics have shifted, and the previous tight balance between supply and demand, which had resulted in higher prices in 2022, has now transformed into a surplus of supply that is responding to the increased prices. At present, natural gas production has gone up by 4% compared to a year ago. According to the EIA’s estimates, the amount of gas stored for work purposes was 2,063 Bcf on Friday, April 28, 2023. This marks a net increase of 54 Bcf from the prior week. As compared to the same period last year, gas stocks were higher by 507 Bcf, and they were 341 Bcf above the five-year average of 1,722 Bcf. The current total working gas of 2,063 Bcf falls within the historical range of the past five years. However, The Energy Information Administration has released a report stating that the total consumption of gas in the United States has decreased from 73.8 Bcf per day for the week ending April 5 to 69.6 Bcf per day for the week ending April 12, which represents a 5.7% decline. The primary reason for this drop in consumption was due to a reduction in demand from the residential and commercial sectors, which fell by 3.9 Bcf per day from 22.8 Bcf per day to 18.9 Bcf per day during the week ending April 12. This decline of 17% can be attributed to the rising temperatures observed across the country. F&D Partners is advising its clients to opt for a fixed-rate plan, citing the forthcoming warmer weather, decrease in demand, and increase in production as factors contributing to a reduction in the risk of price hikes.

According to the EIA’s Natural Gas Weekly Update, there was a slight week-over-week increase in dry gas production, from 100.6 Bcf per day to 100.7 Bcf per day, during the week ending on April 12. While this increase may seem minimal, it should be noted that dry gas production has gone up by 4.7 Bcf per day when compared to the figures from a year ago.

It is anticipated that the Henry Hub natural gas spot price in the US will remain steady at an average of $2.65/MMBtu for the second quarter of 2023. This is due to the fact that natural gas prices typically go down during spring as the demand for natural gas for space heating reduces when temperatures become more moderate. However, this year, the weather has been spring-like from the start, which has led to a decrease in natural gas consumption during the first two months of the year as compared to the levels of both the previous year and the previous five years, thereby resulting in a drop in natural gas prices.

Looking ahead, it is expected that the US natural gas production will remain relatively stable, while there will be a surge in demand for feed gas from Freeport LNG due to the export terminal resuming full operations. Furthermore, there will be an increase in natural gas consumption in the electric power sector, which will result in an increase in natural gas prices throughout the summer. The prediction is that the Henry Hub price will average slightly above $3.00/MMBtu in the third quarter of 2023.

The NYISO’s Summer 2023 capacity strip auction results were released on April 3, 2023, with NYC capacity strips settling at $17.75/kW-month after two years of low pricing. One of the reasons for the tightening capacity market is the DEC Peaker Rule, which established maximum emissions rates of nitrous oxides during the ozone season. The first tranche of these regulations came into effect in May 2023, which will force affected peaking units to comply with emissions controls, cease operations during the ozone season, or retire altogether. According to NYISO’s 2022 Reliability Needs Assessment, about 238 MW of summer capability capacity in Zones J and K will be out-of-service from May 1, 2023, to comply with the DEC Peaker Rule. Retail electricity customers’ capacity costs in NYISO depend on whether they receive supply from their utility or a third-party supplier. For third-party supply customers, capacity costs can be fixed for a predetermined term or passed through based on where spot prices settle.

In the past few months, March and April, the index prices have been falling significantly. In fact, March and April have seen a decline of 34% and 40% respectively, compared to the prices of the previous month. This is after the colder February when prices spiked to over $50/MWh. However, with the arrival of seasonal temperatures, it was expected that April would finish up in the low $30s.

In PJM territory, index electricity prices are showing a consistent decline due to mild weather conditions, with hourly prices following the downward trend. This year’s prices in 2023 appear similar to the pricing patterns observed in 2017 and 2019, which could indicate that power consumption levels may be returning to pre-Covid levels. On the other hand, there is little movement in the forward strips for natural gas prices on a month-over-month basis due to a lack of significant changes in gas fundamentals, leading to low price volatility during the shoulder month. The high storage levels and anticipated increase in LNG export capacity next year are important factors to consider when predicting natural gas prices in the coming months. Natural gas index prices are also decreasing steadily due to low demand, with Q1 2023 prices being the lowest since 2016, excluding the COVID-impacted year of 2020. Moderate temperatures, which reduce the need for natural gas for space heating, are among the factors contributing to the decrease in demand. As April temperatures continue to become milder, it is anticipated that the decreasing trend will continue, with prices expected to settle below $2/Dth.

According to EIA, natural gas inventories in the United States will see an increase of 1,985 Bcf during the injection season of April through October, which is in line with the summer injection averages of the past five years. This increase will lead to a rise of 8% in inventories as compared to the stocks at the end of October in the previous year. At the end of October 2023, inventories are expected to reach 3,842 Bcf, which is 6% higher than the five-year average. However, the actual inventories will be impacted by summer temperatures. In case of a warmer summer, natural gas consumption in the power sector would increase, resulting in less gas in storage and upward pressure on prices. Conversely, cooler summer weather would decrease consumption, increase storage, and put downward pressure on prices.

F&D Partners was very successful in navigating one of the most volatile years in the energy markets by helping our clients save tremendously.

Contact us today for the newest strategies in the energy markets for 2023, 2024 and 2025.