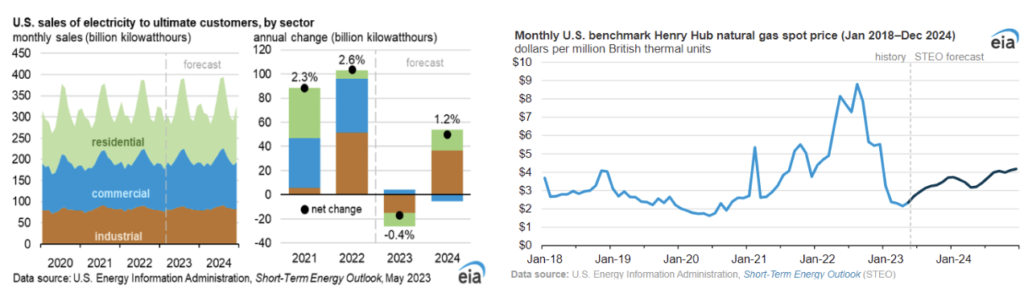

In the May Short-Term Energy Outlook (STEO), it is anticipated that the U.S. benchmark Henry Hub natural gas spot price will experience an upward trend throughout 2023, following a period of low prices. The average price in April was $2.16 per million British thermal units (MMBtu). The monthly average Henry Hub price is projected to reach $3.71/MMBtu in December. Despite this increase, the forecasted prices for the rest of the year remain significantly lower compared to last year. The average price for the year is expected to be $2.91/MMBtu, marking a decline of more than 50% from the 2022 average price of $6.42/MMBtu. This is because during the 2022-2023 winter, the Henry Hub spot price decreased due to milder temperatures across most of the Lower 48 states, resulting in reduced demand for natural gas for heating purposes and lower withdrawals from storage.

At present, natural gas spot prices experienced declines at various locations during the reporting week (Wednesday, May 17 to Wednesday, May 24). The changes in prices at major pricing hubs ranged from a decrease of 95 cents/MMBtu at PG&E Citygate to an increase of 42 cents/MMBtu at the Waha Hub. The price fluctuations were relatively minor in most trading markets. In the Northeast, the largest price drop occurred at the Algonquin Citygate, serving Boston-area consumers, with a decline of 7 cents. Natural gas consumption in the Northeast decreased slightly, driven by reduced power sector consumption but partially offset by higher residential and commercial sector consumption. West Coast markets saw price decreases, including PG&E Citygate in Northern California, SoCal Citygate in Southern California, and Sumas on the Canada-Washington border. However, the Waha Hub in West Texas experienced a price increase. Maintenance on the Permian Highway Pipeline in West Texas has been completed, restoring its capacity and therefore affecting the price. The U.S. benchmark Henry Hub natural gas spot price is anticipated to rise to around $3.00/MMBtu in July and August, when power demand peaks. In light of these circumstances, F&D Partners strongly advises their clients to seize the opportunity and choose an all-in fixed rate while the prices remain this low.

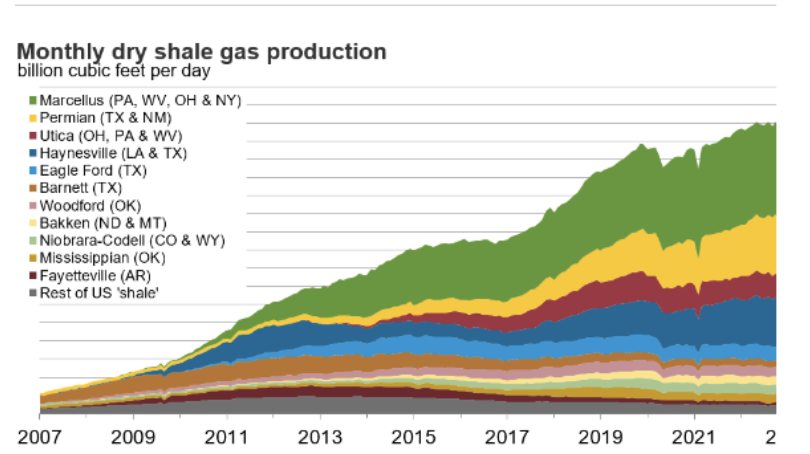

U.S. dry natural gas production experienced growth during the 2022-2023 winter period, reaching a monthly average record of 101.5 billion cubic feet per day (Bcf/d) in February 2023. By the end of April, U.S. natural gas in storage was 19% above the previous five-year average, standing at 2,114 billion cubic feet (Bcf). The expectation is that natural gas storage inventories will remain above the five-year averages throughout 2023, contributing to the projected lower prices compared to the previous year. According to the EIA, as of Friday, May 19, 2023, the estimated working gas in storage stood at 2,336 Bcf, signaling a net increase of 96 Bcf compared to the previous week. In comparison to the same period last year, stocks were higher by 529 Bcf, surpassing the five-year average of 1,996 Bcf by 340 Bcf. The current storage level of 2,336 Bcf falls within the historical range of the past five years.

Turning to demand, total U.S. consumption of natural gas declined by 1.8% (1.2 Bcf/d) compared to the previous report week. Notably, natural gas consumption for power generation experienced a significant drop of 5.8% (1.9 Bcf/d). On the other hand, residential and commercial sector consumption witnessed an increase of 5.0% (0.5 Bcf/d), while the industrial sector saw a smaller uptick of 1.0% (0.2 Bcf/d). During the summer months, the United States typically uses more natural gas for generating electricity as people increase their air-conditioning usage in response to warmer temperatures. The high usage of natural gas for electricity generation this summer is influenced by several factors. Firstly, there has been a decrease in coal-fired electricity generation. Additionally, natural gas prices are relatively low, contributing to its preference as a fuel source. Furthermore, our forecast predicts an overall increase in electricity generation due to the anticipated warmer-than-normal temperatures. Another significant reason why we do not expect natural gas consumption to reach a new peak in 2023 is the greater generation of electricity from renewable sources compared to the previous year. Looking ahead to the summer of 2024, our forecast indicates a 2% decline in natural gas consumption for electricity generation, averaging around 37 billion cubic feet per day (Bcf/d). This decrease is mainly driven by the continued growth of renewable electricity generation sources that are expected to come online throughout 2023 and 2024.

During the final week of May, power forwards experienced a decline of $2/MWh for the 12-month strip. In the NYISO market, UCAP (Installed Capacity) saw an increase across all zones for the upcoming capability periods. However, it is worth noting that the capacity market in New York City continues to face challenges with limited liquidity. The U.S. average residential retail electricity price for this summer is projected to be 16 cents/kWh, indicating a 2% increase compared to the previous summer, according to our forecast. This nominal price hike is slightly below the expected 3% summer-over-summer inflation rate. In the New England states, retail electricity prices rank among the highest in the country, and we anticipate that during summer 2023, the average retail prices in this region will reach 27 cents/kWh, reflecting an 11% increase compared to the previous summer. The main driver behind this anticipated price surge is the relatively elevated natural gas prices in the region compared to other areas of the country. The New England power market experienced extraordinarily cold winter weather, which, along with limited natural gas pipeline capacity, contributed to upward pressure on natural gas prices, consequently impacting regional electricity prices.

Given these conditions, F&D Partners has been recommending their clients an Index + Capacity + Fixed Adder pricing strategy, where index and capacity are let flow with the market and everything else is fixed.

For the PJM territory, energy prices in the first three months of 2023 decreased significantly compared to the same period in 2022. The average price per MWh dropped by $23.85, a decrease of 44.1%. This reduction was mainly due to lower fuel, emissions allowances, and consumables costs, accounting for $14.15 per MWh (59.3% of the decrease). Both coal and natural gas prices were lower in the first three months of 2023. Additionally, the average load during this period decreased by 5.1%, from 92,007 MWh to 87,311 MWh.

The total price of wholesale power also experienced a significant decline, going from $81.84 per MWh in the first three months of 2022 to $53.45 per MWh in the same period of 2023, a decrease of 34.7%. Energy, capacity, and transmission charges are the primary components of the total price, comprising 96.6% of the total price per MWh in the first three months of 2023. The latest projections indicate that the average on-peak power prices at the PJM Western Hub for 2023 are expected to be approximately $47.60 per megawatt-hour (MWh), which represents a decrease compared to the previously forecasted price of $56 per MWh in the January outlook.

Although the average Henry Hub price is predicted to be less than $4.00/MMBtu in 2023, an increase in natural gas demand is anticipated to push prices higher from their recent lows of around $2.00/MMBtu. It is forecasted that natural gas consumption for U.S. electricity generation during the summer months (May-September) will average 38 Bcf/d, the second-highest on record, surpassing last year’s figures. Additionally, U.S. liquefied natural gas (LNG) exports are expected to rise from an average of 11.6 Bcf/d in the first quarter to 12.2 Bcf/d during the summer. The projection for U.S. dry natural gas production is a decline from recent highs, averaging 100.4 Bcf/d in the summer.

As a result of increased demand and reduced production, it is expected that less natural gas will be injected into U.S. storage during the summer, leading to storage inventories closer to the five-year average. The injection season (April 1-October 31) is projected to conclude with inventories 4% higher than the five-year average, reaching 3,762 Bcf.

On the other hand, it is anticipated that the total consumption of electricity in the United States in 2023 will remain similar to that of 2022. A slight decrease in forecasted sales of electricity to residential customers is expected compared to the previous year. This decline in residential electricity demand is primarily attributed to milder winter temperatures, with a projected reduction of 7% in U.S. heating degree days compared to last year. For the upcoming summer, residential electricity demand and bills are expected to be comparable to or slightly higher than the previous year. This is due to similar summer temperatures being offset by higher residential electricity prices.

F&D Partners was very successful in navigating one of the most volatile years in the energy markets by helping our clients save tremendously.

Contact us today for the newest strategies in the energy markets for 2023, 2024 and 2025.