NATURAL GAS

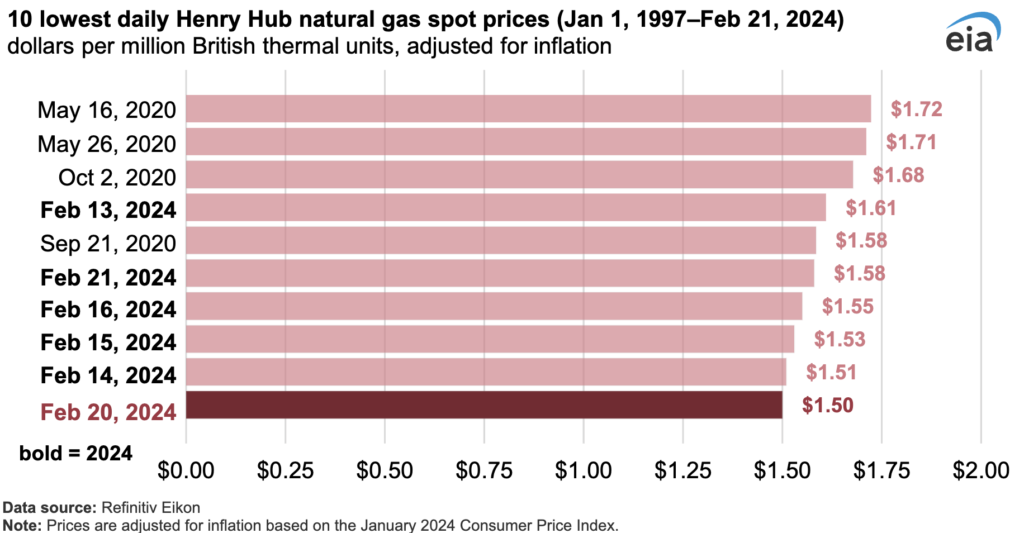

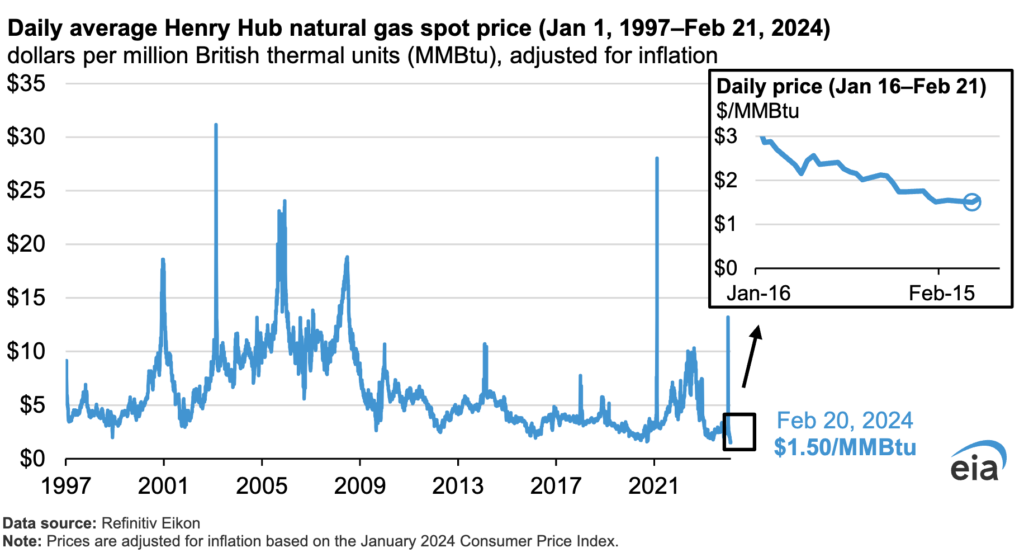

On February 20, 2024, the daily price of natural gas at the U.S. benchmark Henry Hub hit $1.50 per million British thermal units (MMBtu), marking the lowest inflation-adjusted price since at least 1997, as per data from Refinitiv Eikon. Factors such as increased natural gas production, reduced consumption, and higher inventories compared to the previous five-year average (2018–22) led to a decline in prices throughout 2023 and the first two months of 2024.

In December 2023, U.S. dry natural gas production reached a record high of 105.7 billion cubic feet per day (Bcf/d), according to data from S&P Global Commodity Insights, with production remaining robust despite a brief dip during mid-January due to winter storm Heather. Since January 26, production has consistently hovered above 104.1 Bcf/d. Meanwhile, natural gas consumption in the residential and commercial sectors during the current winter heating season (November 1, 2023–March 31, 2024) averaged approximately 5% lower than the five-year average (2019–23), at 35.8 Bcf/d. The surplus in production coupled with reduced consumption has led to decreased withdrawals from storage this winter.

As of the week ending February 16, U.S. working natural gas inventories were on average 12% higher than the previous year and nearly 22% above the five-year average (2019–23), according to the Weekly Natural Gas Storage Report. These elevated storage levels indicate an oversupplied market, contributing to the downward pressure on natural gas prices.

The Henry Hub spot price rose by 3 cents to $1.63/MMBtu on February 27th, while March 2024 NYMEX futures dropped by 16 cents to $1.615/MMBtu. However, April 2024 NYMEX futures increased by 2 cents to $1.885/MMBtu, and the 12-month strip climbed by 9 cents to $2.817/MMBtu.

During the week of February 21-28, natural gas spot prices varied across regions, with decreases on the West Coast and increases elsewhere. Prices ranged from a $0.72/MMBtu drop at PG&E Citygate to a $0.15/MMBtu increase at Eastern Gas South. Most U.S. markets remained below $2.50/MMBtu on February 27th. In the Northeast, prices rose due to colder forecasts despite a 17% decrease in weekly consumption. Algonquin Citygate prices increased from $2.35/MMBtu to $2.46/MMBtu, while Tennessee Zone 4 Marcellus and Eastern Gas South prices also rose. Residential and commercial sector consumption decreased by 25%, and production fell by 3%. Conversely, West Coast prices declined, with Northwest Sumas, PG&E Citygate, and SoCal Citygate experiencing drops. Western region consumption decreased by 3%, and high storage inventories contributed to lower prices.

In West Texas, Waha Hub prices fell by 33 cents, reaching $0.43/MMBtu on February 27th. Capacity reductions due to force majeure led to decreased westbound operational capacity through the Gila and Casa C constraints.

The dynamics of natural gas supply and demand in the United States also revealed notable shifts. According to data from S&P Global Commodity Insights, the average total supply of natural gas experienced a decline of 1.8% (2.0 Bcf/d) compared to the previous report week. This decline stemmed from a decrease in dry natural gas production by 1.1% (1.1 Bcf/d), averaging 102.7 Bcf/d, coupled with a 15.5% (0.8 Bcf/d) reduction in average net imports from Canada. Conversely, demand for natural gas witnessed a significant decrease, with total U.S. consumption falling by 13.3% (12.9 Bcf/d) compared to the previous report week, as reported by S&P Global Commodity Insights. Residential and commercial sector consumption recorded a substantial decline of 24.9% (9.9 Bcf/d), attributed to higher temperatures during this report week compared to the preceding one. For power generation, natural gas consumption decreased by 6.0% (1.9 Bcf/d), while industrial sector consumption declined by 4.4% (1.1 Bcf/d). Exports to Mexico saw a modest reduction of 1.4% (0.1 Bcf/d) and deliveries to U.S. LNG export facilities (LNG pipeline receipts) averaged 13.9 Bcf/d, indicating a slight increase of 0.3 Bcf/d compared to the previous week.

For the week ending February 23, net withdrawals from storage amounted to 96 Bcf, contrasting with the five-year (2019–2023) average net withdrawals of 143 Bcf and last year’s withdrawals of 79 Bcf during the same period. Working natural gas stocks totaled 2,374 Bcf, marking a 27% surplus compared to the five-year average and a 12% increase from the previous year. According to The Desk survey of natural gas analysts, estimates for the weekly net change ranged from net withdrawals of 78 Bcf to 96 Bcf, with a median estimate of 86 Bcf. The current withdrawal rate from storage is 18% lower than the five-year average during the withdrawal season (November through March). If this rate continued, the total inventory on March 31 would reach 2,131 Bcf, surpassing the five-year average of 1,633 Bcf for that time of year by 498 Bcf.

In 2024, it is anticipated that natural gas consumption will grow across all sectors except the industrial sector, where a slight decrease is expected. Sectoral shifts in consumption are primarily influenced by weather conditions, with natural gas-fired power plants supplying approximately 40% of U.S. electricity annually, making electricity demand a significant factor. It is projected that there will be an 11% increase in U.S. natural gas consumption for electricity in 2024 compared to the previous five-year average. Additionally, colder winter temperatures directly impact natural gas consumption in residential and commercial sectors, with combined consumption expected to rise by 5% in 2024 due to warmer-than-average temperatures in January and December 2023. The evolving energy mix, particularly the integration of solar and wind power, will affect natural gas consumption in the electric power sector. Anticipated new LNG terminals, including Golden Pass and Corpus Christi Stage III in Texas and Plaquemines LNG in Louisiana, may influence LNG export forecasts and overall natural gas demand expectations. Despite a U.S. Department of Energy announcement pausing LNG export determinations to certain countries, capacity additions through 2025 remain unaffected. High natural gas prices in Europe and Asia are expected to sustain demand for U.S. LNG, especially amid limited global LNG liquefaction capacity additions, positioning the United States to meet incremental growth in global demand.

ELECTRICITY

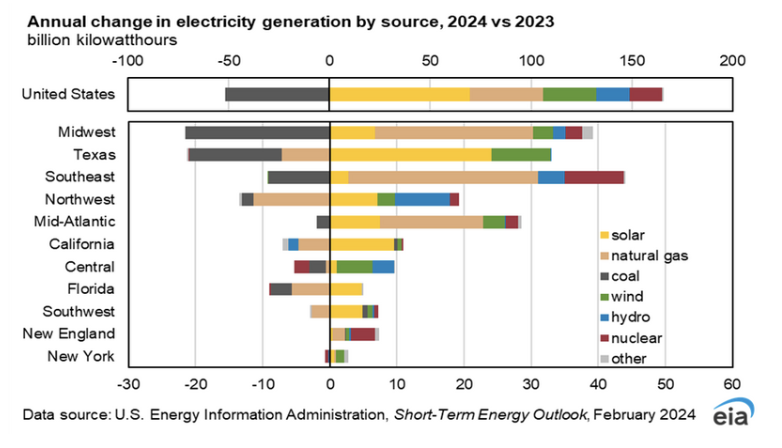

The mix of energy sources used for generating electricity in the United States is evolving, with a steady shift to renewable energy resources and away from fossil fuels. It is expected that solar power will account for the most growth in electricity generation in 2024, driven by a 36-gigawatt increase in solar generating capacity. In the forecast, the U.S. electric power sector is expected to generate 43% more electricity from solar in 2024 than in 2023, an increase of 70 billion kilowatthours (BkWh). U.S. wind generation is forecasted to grow by 6% (26 BkWh), following a slight drop in 2023 due to lower average wind speeds, mostly in the Midwest. U.S. hydropower generation is projected to grow by 7% in 2024 (17 BkWh) due to slightly higher water supply levels, particularly in the Northwest, compared to last year.

The strong growth in renewable generation in 2024 results in slower growth or declines in electricity generation from fossil fuel sources in the forecast. It is expected that U.S. natural gas generation will grow by 2% (37 BkWh) this year, compared with growth of 7% (109 BkWh) in 2023. Generation from coal-fired power plants is likely to continue falling, with a forecasted decline of 8% (52 BkWh) in 2024.

Generation from renewable sources is expected to grow in every region of the United States as a result of new generating capacity scheduled to come online this year. Solar and wind power are expected to grow the most in the portion of Texas that is part of the electric grid managed by the Electric Reliability Council of Texas (ERCOT). Solar generation in ERCOT is forecasted to grow by 90% in 2024 (24 BkWh) and wind generation by 8% (9 BkWh). U.S. coal generation is expected to continue to decline as generation from natural gas remains competitive, some coal plants retire, and more renewable energy sources come online.

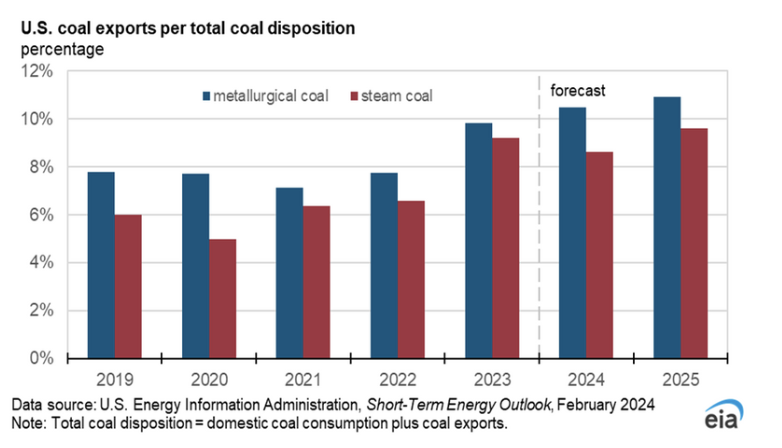

In January 2024, U.S. coal consumption in the electric power sector surged by almost 50% from December 2023, driven by cold temperatures across a significant portion of the country. However, despite this increase, it is expected that coal consumption by the power sector will decrease by 7% in 2024 on an annual basis, followed by a further 6% decline in 2025. This downward trend is attributed to the introduction of new solar and wind generating capacity and the scheduled retirement of 11 gigawatts of coal-fired plant generating capacity. Although coal consumption is projected to decrease over the forecast period, the anticipated 6% decline in 2025 is less than the previously expected 8% decline. This adjustment is influenced by the forecast of slightly more electricity generation and slightly fewer renewable capacity additions compared to previous estimates. Coal production is forecasted to decrease by 19% in 2024 due to a drop in domestic consumption and declining inventories. Further, coal production is expected to decrease by an additional 3% in 2025. As domestic consumption decreases, foreign consumption of U.S. coal is expected to represent a larger proportion of the total disposition of U.S. coal in 2025, despite a projected 7% decrease in exports to 95 million short tons (MMst) in 2024, followed by a stabilization near that level in 2025. Exports are anticipated to constitute 20% of the total disposition of U.S. coal by 2025, up from 14% in 2022 and 19% in 2023.

The same reporting week, despite a lack of heating demand, strong production, and expanding gas storage surpluses compared to last year and the five-year average, forward power prices in the Mid-Atlantic Region rose. Natural gas prices saw an increase as traders likely sought profits following a previous sell-off in NYMEX prices. Recent overnight models indicated diminishing heating demand as we closed the warmest winter on record since 1950. While there may still have been some colder days, the overall pattern remained warmer than normal. Power forwards for the 2024-2028 term in the Mid-Atlantic region were up by 3% over the past week. Meanwhile, the month-to-date day-ahead average settlement price for February in West Hub stood at $24.73/MWh, marking a 43% decrease from January’s average settlement price. Regarding PJM’s 2025/26 Capacity Auction, FERC approved a delay from June to July to accommodate market participants’ requests for additional time to understand the new Effective Load Carrying Capability (ELCC) methodology, recently approved by PJM. This slight delay aimed to give market participants more time to assess the impact on unit-specific offer cap submissions, pushing the auction to July 17th along with a postponement of associated pre-auction deadlines.

On the other hand, The Great Lakes Region’s forward power prices remained steady this week despite a rise in natural gas prices, driven by traders seizing opportunities in the market and anticipating potential production cuts due to extremely low prices. Currently, we’re experiencing an amplified weather pattern: a warming ridge in the Mid-con and East, contrasting with a cooling and stormy trough in the West. This setup has brought record high temperatures under the ridge and record rainfall/snow in the West. As the week progresses, the jet stream will begin to flatten out, leading to a brief cooldown in the eastern U.S. by the weekend, accompanied by fewer storms and cooler weather in the West. Power forwards for the 2025-2028 term in the GLR region saw minimal change throughout the week. The final day-ahead average settlement price for February in AdHub was $20.64/MWh, marking a 26% decrease from January’s average, while COMED averaged $16.78 for February, 32% lower than the previous month.

Governor Hochul of New York recently announced conditional awards for two offshore wind projects, totaling over 1,700 MW, through NYSERDA’s fourth offshore wind solicitation. This fast-tracked process was initiated to fill the gap left by terminated projects following the PSC’s decision in October 2023. The awarded projects, Empire Wind 1 and Sunrise Wind, were originally seeking cost increases, prompting them to cancel their existing contracts and rebid. These projects are expected to begin operations in 2026, providing electricity for about 10% of New York City’s and Long Island’s needs. The development cost is around $150/MWh, adding approximately $2 per month for consumers, compared to the prior agreement’s potential increase of 73 cents per month. A third bidder, Community Offshore Wind 2, is on a “waitlist” for potential future award. This announcement highlights New York’s commitment to the Climate Leadership and Community Protection Act’s goal of 9,000 MW of offshore wind energy by 2035. A public webinar on the re-awards is scheduled by NYSERDA for March 19th.

F&D Partners was very successful in navigating one of the most volatile years in the energy markets by helping our clients save tremendously.

Contact us today for the newest strategies in the energy markets for 2024 – 2028.