This February, natural gas and electric prices continued to experience volatility. Natural gas prices have continued to fall, whereas electric prices skyrocketed to nearly 18 cents per kWh in New York. Warmer than average weather allowed for a small withdrawal of 71 Bcf (Bcf =Billion cubic feet: standard unit of measurement for natural gas supply/demand) from underground LNG storage on the week ending February 17th, leaving storage levels 15.2 percent above the 5-year- average and 21.9 percent above the previous year. Due to increasing production in 2022 to make up for the losses brought on by the epidemic, decreased demand continued to contribute to low pricing together with high supply. February temperatures in the US were the mildest since 2006, which resulted in reduced consumption of natural gas for space heating by a significant margin. An expected drop-in manufacturing activity this year also contributed to reduced demand for natural gas. In February natural gas prices remained below $3.00 MMBtu and ended the month slightly

above $2.60 MMBtu. As the spring comes closer, potential for price spikes diminish as warmer weather is well on its way and storage inventories remain well above the 5-yearaverage. With storage levels well above the five-year- average and production at an all-time high, F&D Partners recommends our clients fix their natural gas prices as we may not see prices come this low again.

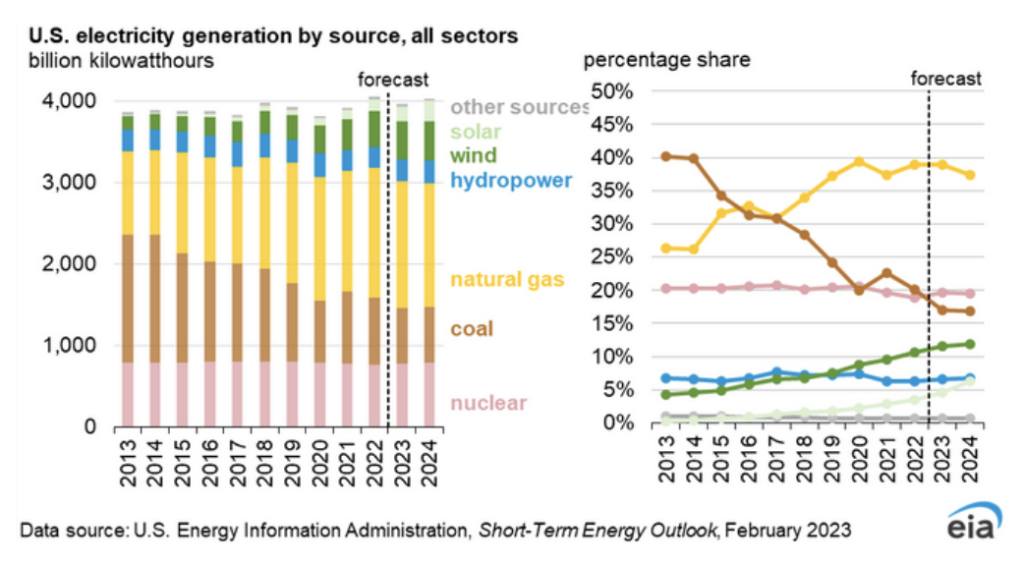

Furthermore, because more power is being produced from renewable resources, there has been a decrease in natural gas use. Natural gas use in power generation is currently set to fall by 2 percent in 2023 as more photovoltaic capacity comes online. Dry natural gas production continues to remain high at slightly over 100 Bcf/d in February, outpacing demand. This February natural gas production averaged 99 Bcf/d, down 1.0 Bcf/d month-over-month. The return of the Freeport LNG terminal sometime in 1Q23 will likely add 2 Bc/f of natural gas demand to the U.S market once fully operational. The Freeport terminal has performed a safety review of liquification train 1 and completed the corrective work necessary to safely restart the unit. Train 2 is also in the process of restarting after receiving approval from the Federal Energy Regulatory Commission grated last week. Train 3 was safely restarted and is currently producing LNG for export. Electricity prices surged significantly throughout February due to increased demand.

Electricity produced by renewable resources is expected to rise from 22 to 24 percent while the EIA expects a 2 percent decline in US electric power generation. The addition of 63 GW of utility-scale solar generating capacity is responsible for the gains in the share of renewable energy that will enter service by the end of 2024. The new generating capacity is expected to reduce the output from fossil-fuel fired plants. More buildings are also installing

heat pumps and making the necessary upgrades to make their buildings more efficient in order to reduce emissions, increasing demand for electricity, allowing the United States to shift away from gas. F&D Partners is looking at strategies for different clients of either an index with fixed retail adder strategy where the wholesale price of energy flows with the market, and the taxes, line loss, ISO fees, and ancillary services are fixed, or a short term all-in

fixed rate.

On February 1st, Governor Hochul introduced a $227 billion spending plan during her Executive Budget Address, a 2.4 increase from 2022. An economy-wide cap-and-invest program will be implemented by the Department of Environmental Conservation (DEC) and NYSERDA. The Governor explained that the program’s goal is to establish a gradually declining cap on greenhouse emissions, limit the financial impact of New Yorkers, and invest proceeds in programs that help reduce emissions while maintaining the competitive nature of the State’s industries. In the Washington D.C. area electricity prices remain lower than the national average price per kWh. Despite the drop in natural gas prices after the holiday season and into 1Q23, prices per kWh continued to remain high and are expected to increase more during the winter due to high demand. The price per kWh in Washington D.C. is 15.5 cents, only slightly below the national average of 16.8 cents per kWh. Washington DC’s prices remain high because it imports most of its energy, making its demand 80 times higher than its supply. Utility (piped) gas remains high at $1.834 per therm because of the many houses that use

gas for heating. According to CME Group, the Henry Hub Natural gas futures are below $3.5 MMBtu throughout spring and summer 2023, and remain slightly over $2.7 MMBtu for the remainder of the winter. Natural gas futures reached a low of $2.732 for April 2023. Natural gas futures are expected to go over three during the end of the spring, when the Freeport LNG terminal is scheduled to be fully operational, bringing 2.3 Bcf/d of demand back to the

market.

F&D Partners was very successful in navigating one of the most volatile years in the energy markets by helping our clients save tremendously.

Contact us today for the newest strategies in the energy markets for 2023, 2024 and 2025.